Posted April 14, 2026

Mandatory Roth Catch-Ups: 5 Things High Earners Should Be Thinking About Now

If you are 50 or over and contributing to your 401(k), a key rule has changed how you save—and how you’re taxed.

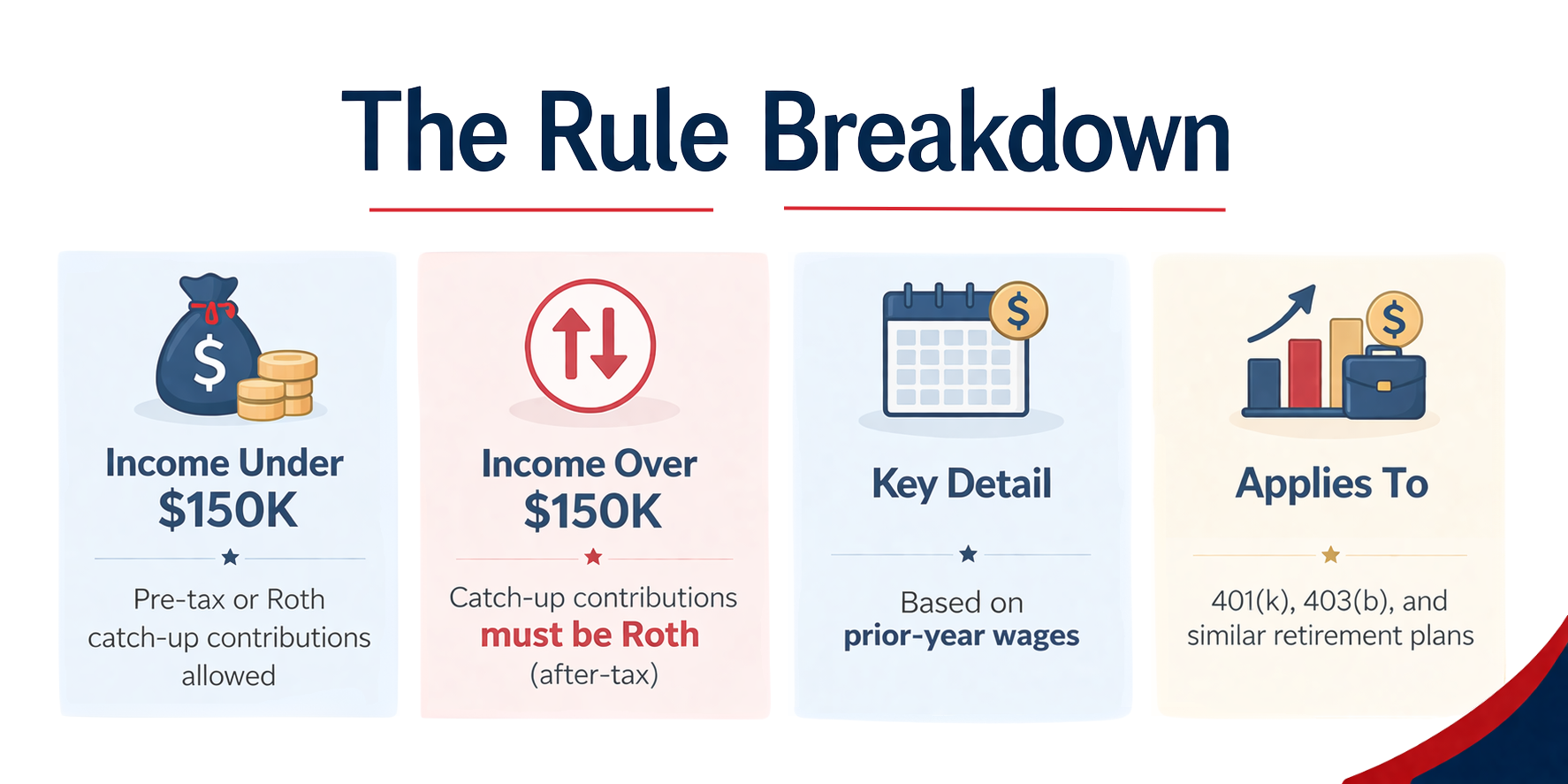

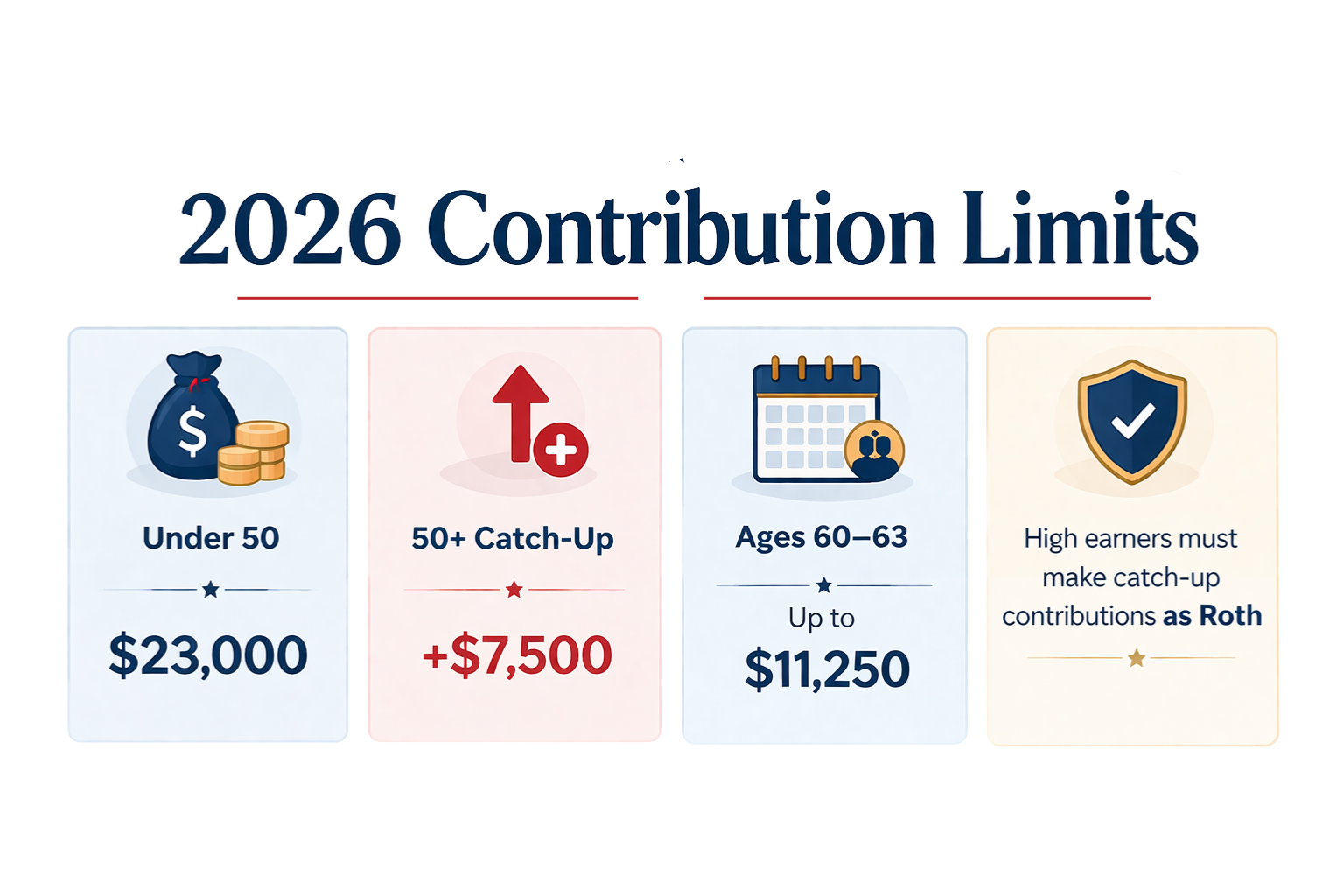

As of January 1, 2026, under SECURE 2.0, high earners can no longer make catch-up contributions on a pre-tax basis.

Now, those contributions must be made as Roth (after-tax).

That may feel like a loss of a valuable tax break. In reality, it’s a shift in when you pay taxes—and that opens the door to smarter planning.

What it Means

- Pre-tax → Tax break now, taxes later

- Roth → Taxes now, tax-free later

Why This Isn’t Just a “Tax Change”

For years, high earners have leaned on pre-tax contributions to reduce taxable income today. Now, that lever gets smaller.

But in exchange, you gain something powerful: tax-free income in retirement.

“Roth accounts are considered the ‘gold standard’ in IRA accounts, so this is a great way for higher earners to have tax-free retirement funds — assuming the tax-free part never changes in the future.”

— Elaine Kirby, CPA, BNA CPAs & Advisors

That perspective highlights an important shift. This change isn’t just about losing a deduction today—it’s about building long-term flexibility and tax-efficient income for the future.

5 Things High Earners Should Be Thinking About Now

1. Your tax bill may go up (in the short term)

Catch-up contributions will no longer reduce taxable income.

2. You’re quietly building tax-free income

Every Roth dollar is:

- Growing tax-free

- Withdrawn tax-free (if qualified)

That’s a built-in hedge against future tax increases

3. This improves tax diversification

Think of retirement income like buckets:

- Pre-tax (taxed later)

- Roth (tax-free)

- Taxable accounts

More Roth = more control later

4. Strategy matters more than ever

This isn’t a “set it and forget it” decision anymore.

You now need to think about:

- Where your income will come from in retirement

- How to manage tax brackets year by year

- When to draw from each account type

5. This is a planning opportunity—not just a rule

The clients who benefit most won’t be the ones who avoid the rule—

They’ll be the ones who plan around it

Contact BNA Wealth Today

If you’re looking for reliable financial guidance, we’re just a call away. Reach out to us at 803.324.7100 or email us at success@bna.com to see how we can support your goals.

BNA Wealth: Smarter Finances, Mastering Wealth Management